We are still in the midst of the Covid-19 pandemic which shows no sign of abating. We need to stay until there are zero cases for some time. Even after 102 days of no cases, , New Zealand experienced another wave. As we consider staying at home and being safe, or carrying on with our lives as before the pandemic, we realise one thing: that the preservation of life must take centre stage. However, how do we take control of our life? We’ve got to ensure we are the person who is standing on this stage because it is our life, it is our stage.

“Life is Fragile, and is not a Rehearsal”

If this pandemic brings home any truths, it would be this: Our time on earth is limited. None of us knows when our final moment will be.

The immediate reaction of those who had contracted the disease might have been:“WHY ME?”. Whenever anyone we know passes away, most tend to say, “So sudden.”. Indeed, many pass away ‘suddenly’.

If you have people who depend on you, you need to ask yourself what you would do for them. What would you do to ensure your sudden, unplanned departure will not hurt them more than it will have emotionally? How can your children continue to have food on the table? Will they still have the kind of education you would have provided to them if you do not leave them “suddenly”?

And since life is not a rehearsal, what would like to do for yourself?

How would you feel if you are positive for Covid-19 case?

Imagine if you are now told that you have contracted Covid-19, and that the chances of you not living through it is high, and you may have only 24 hours left to live? What regrets would you have? Would you think of all the things that you wanted to do, should have done, but did not do? Would you think of all that you had delaying, putting off because you thought you still had lots of time left?

Would you be worried about the performance of the stock market? I highly doubt it.

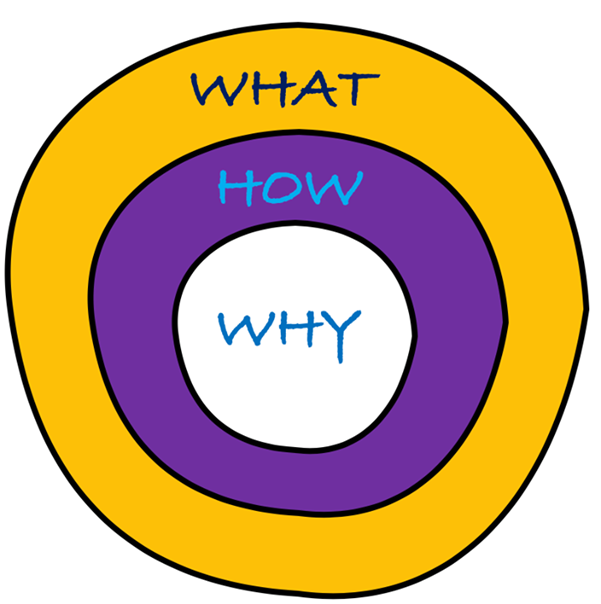

Start with WHY

Try to use the time you have staying at home to ponder the things that are important to you. If you think it is money, let me tell you this: Yes, money is important. It is important to help you do what you want to do in life, but it is not the ultimate thing you want to achieve. Think deeper. Money is just the “what”. We use it to buy something, to do something, to accomplish something. The more important question is “why?”. Why do you want to do this? Why is it important to you? Why do you want to accomplish this so badly? After understanding the why, only then will you have the courage to stick to the plan, and unleash your creativity to find out what the “how” is.

The Golden Circle, Start with Why

Simon Sinek

Have a Conversation on Financial Life Planning

In my work, I wear 3 hats. The first one is the hat of a life planner. This is the part of my job that requires me to understand, and help clients to discover what’s important to them. This is about identifying the value of the client, their principles, etc. This is about helping them to understand they must place value on relationships and health, not money. I think it only makes sense when,based on the WHYs,, we allocate and manage our resources (time, money) to design the life that we want to have. Not the other way around.

The second hat is the hat of a Financial Planner. The financial planner’s job is to get information on the client’s Income, lifestyle, assets, and liabilities. I will then make a projection on their future cash flow, and understand how their current financial behaviour and lifestyle is affecting their ability to realize all their important life goals. I will do scenario-based planning to understand the impact certain unexpected events such as illnesses, retrenchment or change of career will have on their ability to pursue all their life goals. This will helps us to find answers such as if it is ok to upgrade to a bigger house. We can get the answers to many conflicting decisions, and make smarter trade-offs. More importantly, this is when I can help clients to find out if they will have enough to live the life they want to live. So that they don’t have to compromise to live a life that they have to accept.

The third hat is the least important one. This is the hat of a financial advisor. This is where I provide recommendations to a client concerning the products that meet their financial life planning needs. Traditionally, we think that the products are the most important, but I state that the first 2 roles are more important.

Deciding on the products is just like deciding which vehicle to take to travel from point A to point B. However,I think the most important thing should be to define what point B is, and when to make it happen. It is about making sure we have enough fuel to last us through the journey no matter what happens.

Life is not a Spreadsheet

The is just a summary of what you can expect when having a conversation with a Financial Life Planner. Evidently, it is more than just about money or numbers. It is not just about investment returns or the performance of the stock market.

We cannot put our life into an excel spreadsheet and say “I have done my Financial Planning.”

Life is not a spreadsheet. It is fragile, and is not a rehearsal. Why not do something for yourself so that you have no regrets tomorrow?

Sometimes, we need to have an external voice to guide us to discover the answers to these questions. That is why it helps to discuss this with someone who is there to provide you with an objective view, and to coach you to be fearless while taking charge of your life.

If you feel that having a conversation about money and life at this point of time is a good thing to do, I urge you to talk about it today, and not put it off to tomorrow. Take proactive action to make your life happen. Don’t let life happen to you. One more thing. Stay safe. Wear your mask, and put the RM 1,000 you will incur as a fine if you don’t into an investment that will grow in value over time.