Personal Financial Engineering (PFE) refers to the use of mathematical and statistical techniques to solve financial problems systematically, as defined by Investopedia.

This article explains the concept on PFE using 2 case studies for easy understanding.The article also discusses the advantages and benefits gained in the medium to long terms if we have applied the knowledge correctly. In short, PFE should be financially easy to use, technically adaptable and

commercially adjustable.

Due to the Covid-19 pandemic, the Malaysian government has taken various measures to ensure the financial and economic outlook for the next 4 – 6 months remains steady. A moratorium on loan payments has been implemented, something that has not happened in the Malaysian financial market since the 1997 and 2008 financial crises. As such, many uncertainties have arisen and this article will also discuss the financial impacts carefully, using the examples quoted by Bank Negara Malaysia (BNM). We are now in the period of a moratorium on loan payments. Other than a lowering of the OPR as happened recently, both deferment and a lower ELR (effective lending rate) will definitely create more liquidity for both consumers and bankers. Let’s look at this independently. Do consult your financial planner if you need more information and guidance. We will be sharing 2 additional scenarios based on Housing Loan Deferment and Hire Purchase Loan Deferment respectively.

Key Features of Personal Financial Engineering:

Easy to Use: Users like you and I can use the system (financial calculator) easily and it shall be capable of interacting with and advising you if you have some financial concerns to be addressed carefully. Technically Adaptable: Users like you and I can “Act and React” to the market dynamics to address the WHAT IF analysis in a real time manner. For example, if today, BNM reduces the ELR or Effective Lending Rate, What if 1) I choose to keep my

instalments the same as before the reduction; 2) I choose to reduce my instalment as advised; 3) I choose to pay more now, not taking options 1 and 2? Commercially Adjustable: Users like you and I can “Engineer and Re-engineer” our financial plan when one or more of our life’s priorities change due to any reason. For example, we recently experienced a sudden market crash due to the Covid-19 pandemic. How can you capitalize on this window?

Can We Engineer Our Future Financially?

Yes, definitely. We are now dealing with the principle of TVM (Time Value of Money). This explains how TVM relates to 3 basic economic parameters, i.e. Growth, Inflation and Risk.

To put things into perspective, if you are 25 years old now and you think ahead to your being 35 years of age, you could probably engineer more financial results than one who is now 45 yeas old and only has 15 years ahead to plan his finances.

In financial engineering, the first 10-15 years are categorised as the accumulating phase, and the next 10-15 years are categorised as the

accelerating and exponential phase. If we don’t take care during the first 15 years, we will have technically lost the financial advantages in a big way.

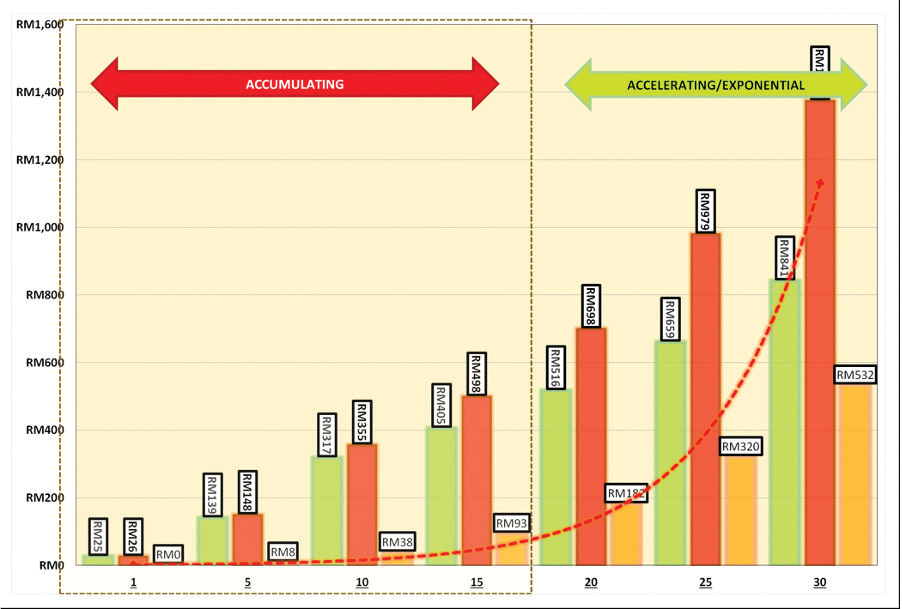

Chart A

- Assuming:

- we invest RM24,000 into a trust fund

- we invest for only 10 years

- we let the portfolio continue to grow and compound

2. Based on 5% as average return and 7% as average return:.

- Green: 5%

- Red: 7%

- Orange: Additional Capital Growth and Gain

Factors and Controls

TVM is a very powerful financial planning concept and it works around key economic parameters, i.e. Growth (G), Inflation (I)

and Risk (R). Growth: Refers to the annual return of an investment vehicle such as FD (“xed deposit) and EPF (Employees Provident Fund). Using EPF as an example, if the average return is 5.5% p.a and for FD it is 3.0% p.a., both vehicles will deliver more or less the same results at 10 years, but will be significantly different at 20 years and exponentially huge at 30 years. This is the power of compounding.

Inflation: Refers to the rise in the general level of prices where a unit of currency e!ectively buys less in the future. In simple terms, RM1 tomorrow will be worth less than RM1 today. By using the rule of 72, if in#ation is 4% p.a, it takes exactly 18 years to half its economic value. Risk: Refers to the associated factors such as financial and non-financial risks but both are financially correlated. For example, if your investment vehicle delivers a bad return over the years, you will accumulate significantly lower returns. Another example is non-financial risks as related to a health crisis. If the bread

winner suers a health crisis such as being diagnosed with a major critical condition or suffers total permanent disability or passes away, we can imagine the potential disaster.

Hence, if we apply the know-how to manage the G, I and R very wisely, we we will not only structure and engineer a sustainable financial result but at the same time mitigate the associated/ unforeseen risks as much as possible. No matter what, we aim to reach our target objectively due to proper financial planning and management.

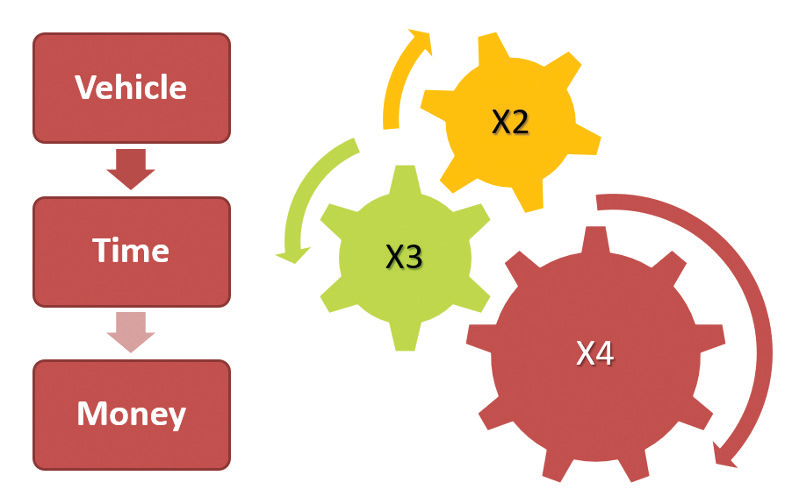

Diagram B:

• Managing the vehicle, time and money is vital because we can achieve favourable financial results (See Chart A) more confidently.

• Our example above was prepared based on 10 years. Imagine today this is a 20/30 years scenario. The “nal harvest will be huge during investment

maturity.

• Vehicle: FD, Bond Fund, Equity Fund, Dividends-Based Fund, etc.

• Time: Commitment to Time to Accumulate and Compound.

• Money: Level/Incremental investment, discipline and consistency.

We Can Achieve Di!erent Financial Results by

2X, 3X or 4X, Using Similar Resources but a Di!erent Vehicle.

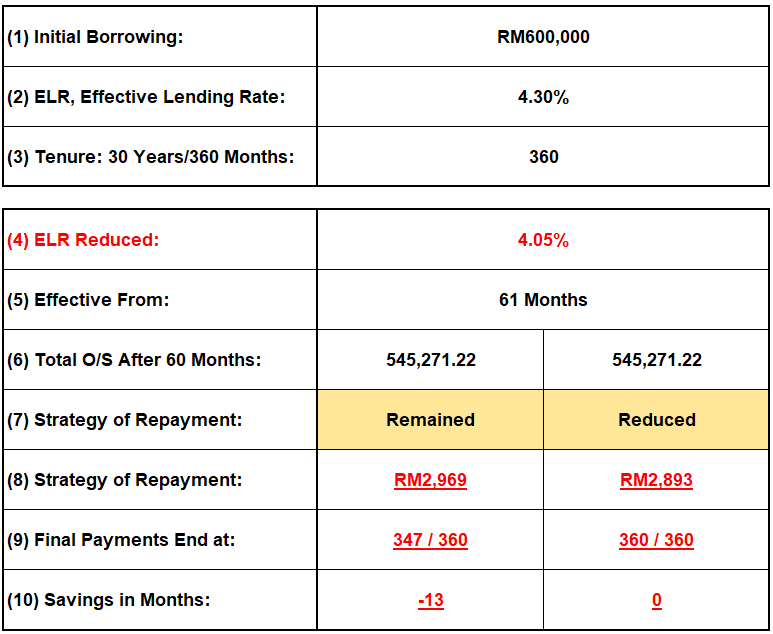

Case Study A

In case study A, we use a real scenario to study the cause and effect using the housing loans category. If your loan has an Initial Borrowing at RM600K, assuming an Effective Lending Rate of 4.3% p.a unchanged for simplicity, Tenure is 360 Months. We have a situation here, assuming OPR is reduced

by 0.25% at 60 months, let’s assess the financial implications carefully. We can use FE to “engineer” the results (before and after) immediately for consideration. (Please note: this is just for explanation purpose; it does not reflect any banks in Malaysia.)

Chart C:

A) What if I choose to let my instalment remain as it is?

B) What if I choose to reduce my instalment as advised?

Repayment strategy when ELR is reduced by 0.25%; repayment remains as before reduction or is reduced.

You Decide:

We could save up to 13 months of additional instalments!