In this new era of 2021, technology has become the most significant tools in our live. Financial Technology (Fintech) has played an important role for the region, country and globalization in financial market. Fintech referred to technology tools enabled to access financial services and products that provided multiple financial services with rapid and efficiency across the world. The innovation of Fintech in financial services and impacts due to rapid growth of Fintech. Meanwhile, emergence of Fintech some positive and some negative significant impacts of Fintech development toward financial industry and also involved other industry such as educations and health industry.

Fintech Evolutions

Fintech 1.0 as first stage started at year 1866-1967. The first stage of evolution focused on global trading. The early stage of evolutions established the global interconnection of banks and financial institutions. Infrastructure structures such as bridges and railroad has been built as strong evidence while supported for trading activities. This stage was important as initial started point to bring forward Fintech innovation in the future. During this period, there was first transatlantic cable and the first electronic fund transfer system developed by USA in 1866 and 1918. Furthermore, Diner club credit card was created on year 1950 which to attract first group of people started to use digital payment though credit card. Obviously, Fintech evolutions started since early stage in developed country. That was the reason why technology more advance in developed country when compared with developing country.

Second stage of Fintech 2.0 started at year 1967-2008 where the financial sector developed and financial services promoted at this period. The first ATM has launched in 1967 and digital world has begun. Also, the world’s first digital stock exchange by NASDAQ in 1971 for trading activities. Fintech 2.0 has significant changed from traditional banking system to become digital system or technology system later. Many financial services activities operated in digital system such as stock market exchanges, bankers’ automated clearing house services, payments system (SWIFT), etc. During this period, many others Fintech has developed and encouraged on Fintech usage such as online banking, mobile payments and PayPal was founded. The internet system and e-commerce business models flourished especially in developed country. At the same times, regulator on protected the Fintech users were established due to rapid growth of technology and issues of Fintech growth. During this stage, financial technology has wider used by individuals, banks and others financial institutions. Traditional banking system almost replaced by Fintech innovations in computerized and digitalized system.

Stage three which Fintech 3.0 was started since 2008 until current, the Fintech evolution emerging to newly financial services and products. Unfortunately, financial crisis happened in 2008 and bad caused to market especially in Europe country. The financial crisis not only affected the global financial industry but also influenced the developed country while Fintech start-up still at the beginning stage for developed country. After the financial crisis incident, financial market required to be more transparency due to consumers cautious about the information and sources that provided from the company. Since then, many companies developed Fintech start-up due to competitive financial services at this period. Such as Bitcoin was released on 2009 and Alibaba introduced SMEs loan on its e-commerce platform. Digital payment growth rapidly in multiple platforms such as Google Wallet, P2P money transferred services and Apple Pay has launched. At the same times, traditional banks faced various challenges while intensive competitive to newly Fintech development. Fintech 3.0 derived on how the forced behind of Fintech innovation to financial sectors throughout the years. Although there were still unclear statements on Fintech issues and various challenges but the emergence Fintech as crucial for financial growth. In other word, financial crisis has bad caused on the emergence market but also created potential possibilities and opportunities on Fintech development for developed and developing country. After understood the Fintech evolutions since traditional transformed to technology; next discussed about Fintech innovation on the financial services and products.

Fintech Innovations

Fintech revolution has gone through the major financial technology revolutions, and now Fintech innovation was encircle the financial services and products, mentioned about the changes, developments, interactions and effectiveness of these new features in financial sectors. Fintech 3.5 defined as fast grew in young populations with equipped mobile devices. Consumers’ behaviour on Fintech usage more to convenience over trust due to Fintech innovations. Many companies and business looked for more opportunities in Fintech start-ups to secure their business with enhanced their products and services. A private sector also involved in this Fintech start-ups to diversify their business and continued grew their business. Scholar studied that financial innovation and sustainable development was a process to understand the customers in financial needs and to offer better financial services and products as far as regulations application. Meanwhile, Fintech innovation defined as ability on understanding, realization and decision making which as a prioritization in financial process. The Fintech innovation showed stronger relations in Fintech evolutions for future trend since there. Moreover, scholar explained that Fintech was simple principle from supply and demand concept on Fintech innovation. Supply factors due to technology advance, regulations, macroeconomic or financial landscape changes and demand factors from all financial services and products such as Fintech payment system. In line with this, developing country such as Taiwan with population only 23 million people but ATM facility available in average every 1.32km. The concept of supply and demand applied to this fact and proved that financial technology innovations occurred from time to time. Furthermore, development of Taiwan’s banking industry with Fintech development in three revolutions started from (1949-1960) defined as embryonic period on the lending markets started; (1961-1989) as second period on developed multiple markets in stocks, bonds and foreign exchange; (1990-2012) defined as consolidation period on globalize and liberalization in digitalization business in financial services in financial sectors. Therefore, the development of financial technology involved individuals, organizations and global aggression, which affected the business development process of the financial industry.

Digital Payment and Business Process Development

Digital payments could be made directly to the financial institutions or indirectly which the Fintech digital payment provided the platforms and payment facilities on payment services combined with technologies. Although users more preferred to the traditional ways which were locals’ banks due to security and private information protected purpose but there were more advantages by using Fintech digital payment. Traditional payment service only could be done according to the different financial institutions method and only has its limitations which according to its own policy and platforms. Example, users always own multiple cards or accounts to access multiple transactions. Meanwhile, digital payments allowed users made multiple transactions that were not specific to any financial institutions policy or dependent on single platform. Digital payment registered with any financial institutions by using technologies and allowed to make multiple transactions independently. Users could easily to make payment or any transactions by selected one of the digital payment services under Fintech providers’ categories. Meanwhile, digital payment was a high-tech, cashless network service that allowed users to shop online. As long as you have a registered account and login name, you could use the digital payment service anytime and anywhere with a password. All shopping would also be delivered to the indicated place and destination. It could be seen that digital payment provided users a fast, convenient, high-tech, convenient consumption anytime, anywhere. Therefore, electronic payment has created the convenience and upsurge of global online shopping.

Digital Payment and Financial Sector in Malaysia

It has been understood that mobile based payment has been gradually replacing the traditional cash-based payment system and it is expected that conventional payment system would be to a great extent replaced by digital payment system with the passage of time. The development of Fintech has created a huge potential for the adoption of digital payment in Malaysia. There were only 127,000 users in Malaysia at year 2005 but increased to 14.4 million at year 2018 on Fintech payment system according Bank Negara Malaysia. The electronic payments as critical component to enable e-commerce and e-trading activities also others financial activities. Enhancement digital payment infrastructure provided fast, convenient and efficient funds transferred on financial development according to Financial Sector Blueprint (Bank Negara Malaysia, 2011). To exploit this potential, the government of Malaysia has set some policy measurement to boost awareness among the Malaysians to follow cashless transaction system. The central bank of Malaysia has formulated a Financial Sector Masterplan (FSMP) which started in 2001. The main objective was to guide and helped in the financial development in Malaysia. The transformation financial sector to new decade played as important role to support local economy growth and built brighten environment to continue competed in the market. Although Malaysia population with 32.6 million, 92.5% Malaysian still liaised on card and cash based transactions.

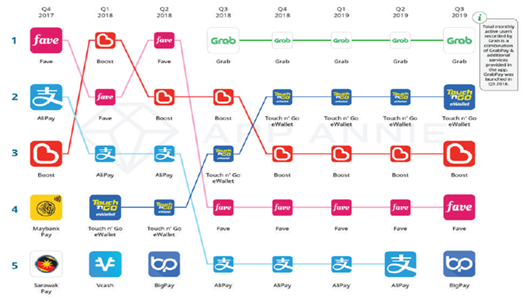

Figure 2.1 Malaysia on E-Wallet Ranking

Sources: https://iprice.my/trends/insights/best-ewallet-malaysia/

Therefore, the development of e-Wallet companies still a new phenomenon in local industry and various cashback program and freebies thrown by the e-Wallet companies to compete in the market. Furthermore, Malaysia government has paid serious actions to promote e-Wallet in cashless industry. Malaysia top e-Wallets companies such as Grab, Touch’n Go and Boost have reach millions of users.Obviously,the efforts of Bank Negara Malaysia in several programs such as reduced the e-payment instant fees and increased the cheque transactions and processing fees. Those actions to digital payment channels and instruments were still in early stage, but significant improved the development of e-payment system in the industry. Electronic wallets have created the convenience and upsurge of global online shopping such as GrabPay, Touch n’Go and Boost as Figure 2.1.

In addition, Malaysia was one of the Asia developing country that has potential significant growth in Fintech start-up. Digital Payment as part of the financial blueprint objectives to help transformed Malaysia to become high value and developed country by providing more secure, faster and cheaper cost environment in financial activities to compete in global market. Digital payment offered high quality of operational on expenditures payments and funds transferred. The bank drove this duty in digital payment adoption in coordinated with central Bank Malaysia. The transaction on digital payment per capital in Malaysia showed double increased from 22 in 2005 to 44 in 2010 while internet banking and credit cards usage increased from 6.3 and 8.2 times respectively. According to the Bank Negara Malaysia report, the financial industry has contributed average 7.3% growth annually of real GDP 11.7% in year 2010 and expected to increase to 10-12% in 2020. Local Banks has increased the total asset from RM3.3 billion from 2002 to become RM240.2 billion at year 2010 showed that the local banks has stronger positions in global market. The development of domestic banks involved Islamic Finance and conventional Banks. Islamic Finance has growth significant form 6% to 22% while sukuk market own 55% on total debt securities market. Today, Islamic financial system provided Islamic fund, Islamic banking and takaful, and became the leader of global Islamic market. Besides that, Malaysia Blueprint program urged the financial institutions became the most important part to integrate with high vale financial system in global market. Financial institutions played as important role in transformations, integrated and implemented the plan towards the missions. At the same time, the transformations affected the transformation from traditional financial system to new technology and advancement environment in providing the financial services and products. Also, the local economy system must change to globalized economy. Hence, the local financial institutions needed to change their traditional business models especially local banks.